Happy Monday Morning!

The Canadian economy grew at an annualized pace of 3.1% in the first quarter, surprising to the upside and trumping the Bank of Canada’s growth forecasts. Four hundred basis points and the economy still hasn’t rolled over. This is prompting calls for the Bank of Canada to move off the sidelines and get back to raising rates once again. Here’s the outspoken chief economist of ScotiaBank, Derek Holt.

Canada’s housing market continues to be on a tear as a combination of very little supply, surging immigration, a return of first-time home buyers, strong job markets, a premature halt to BoC rate hikes and returning FOMO sentiment drive renewed imbalances. I’ve argued since last year that consensus was far too negative toward Canadian housing as it over-emphasized the pressures facing a minority of super- stretched mortgage holders in a classic case of the tail wagging the dog. The broad fundamentals of Canada’s housing market remain highly constructive and will carry ongoing positive spillover effects for consumption as we saw in the Q1 GDP accounts. Recall that home sales were up by 11% m/m Seasonally adjusted in April for the biggest monthly gain since the initial stages of the pandemic recovery in mid-2020 and have risen for three straight months. The city-level data for the month of May looks like momentum will continue. Toronto’s home sales figures for May were up by 5.2% m/m Seasonally adjusted in May and about 25% y/y as listings fell by about 19% y/y but new listings were up by 10% m/m. Prices were up by over 3% m/m SA with the average now at C$1.2 million. Months supply is practically non-existent at 1.3 months.

With Vancouver pending, Toronto adds to evidence of strength in Calgary that posted a record high for all months of May along with a sales-to-new-listings ratio of 85% and months’ supply of just 1 month on tap. One month folks, in both Toronto and Calgary. This country’s policymakers get an ‘F’ for mismanaging housing supply and for serially over-stimulating housing demand and here we go again.

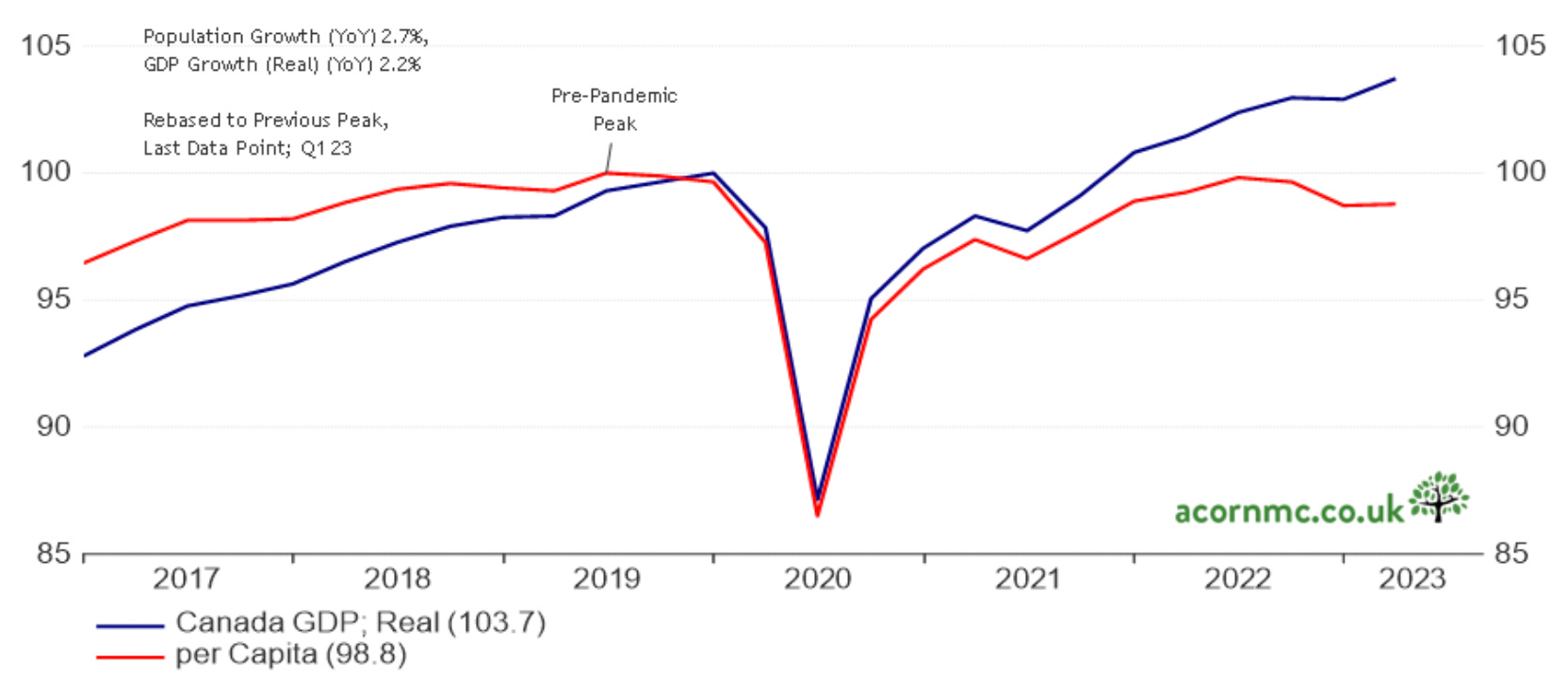

He’s not wrong. As we’ve been covering on this newsletter for several months, eye watering levels of immigration are creating more problems than they’re solving at this point. First of all, it’s creating the illusion of growth. More people, more consumption, the higher nominal GDP goes. In reality, when you look at real GDP per capita there’s been zero growth for nearly five years. In other words, living standards are not improving, which if you pulled most Canadians is probably the answer you’d get.

Record immigration continues to put severe strains on an already tight housing market. Here’s what’s happening in real time right now. This country just added nearly 150,000 permanent residents in Q1 2023, the most on record by a wide margin. This is happening as immigration artificially inflates GDP, prompting the BoC to keep raising rates. Meanwhile, surging interest rates are killing the viability of any new construction. Somehow Ottawa hasn’t figured this out yet. Suffice to say this is setting up to be a giant shit sandwich a few years from now, and we’re all going to have to take a bite.

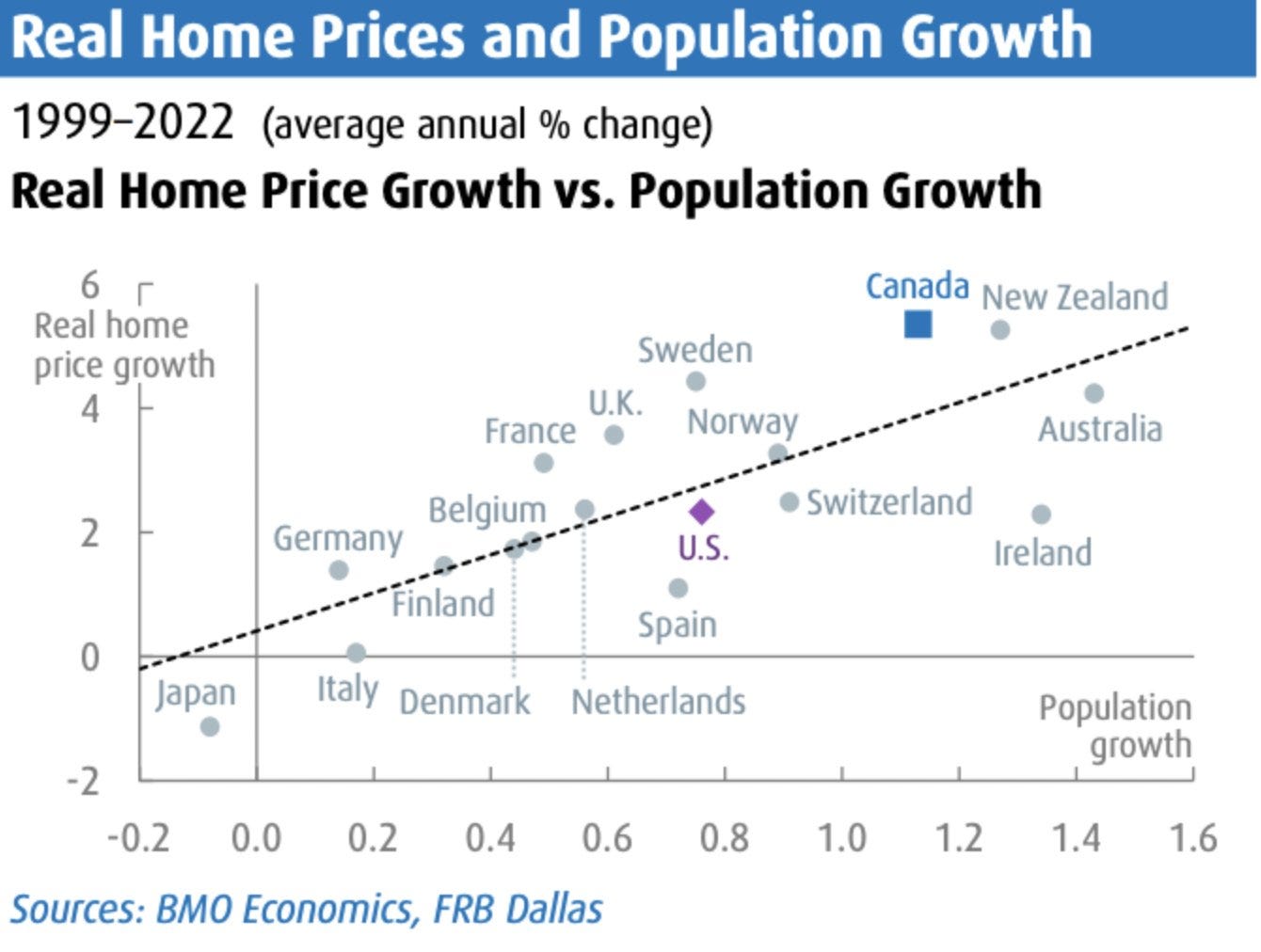

According to BMO, evidence from 18 large advanced economies since the start of the century shows that real home prices are closely correlated with population growth over time. Regression analysis suggests that every 1% rise in population will be associated over time with real home price growth of just over 3% per year (on top of inflation).

No wonder Canadians love speculating on pre-sale condos. They’re betting government incompetence will continue.

Anyways, whether the Bank of Canada raises rates this week or not, what we do know is interest rates will be higher for longer under operation human QE. Variable rate mortgage holders will be the sacrificial lambs and housing starts will continue to go down for the dirtnap.