Happy Monday Morning!

At the beginning of the year I was part of a real estate pannel with REW on the state of the Vancouver housing market. On stage, in front of a live audience, the moderator asked me for my forecast for 2023. I promplty noted at the time that “we’re going to have a year of volatility.”

And that’s exactly what it’s been.

This year has been marked by a record low in home sales, followed by a record low in new listings, and inventory. Against all odds, prices ripped higher in the spring. This prompted the Bank of Canada to hit the panic button and start hiking rates again. Bond yields have followed suit, pushing mortgae rates higher too. Sales have stalled once again, and prices are now following suit. To put it lightly, it’s been nothing short of a roller coaster ride in 2023.

Recent stats from CREA highlight the whipsaw emanating across the nations housing markets. While home sales were officially up 1.9% year-over-year in September across Canada, they were still the third lowest in twenty years. Buyers are squarely on the sidelines with very little urgency considering mortgage rates are hovering well into the 6% range and more favourable mortgage rate holds in the high 4’s and low 5’s have now, largely expired.

The only difference between this September and last September is that new listings last year were at a meager 68K, the lowest total in 17 years. This year listings have bounced 14% and are back in line with long term averages. Inventory is finally starting to build.

In summary, demand remains weak but new listings and inventory are finally growing. This is a receipe for lower prices as we head into the seasonally slower winter months.

So unless mortgage rates fall in a meaninful fashion, the demand picture looks incredibly challenged. Just to give you an idea of borrowing capacity today, assuming you can pick up a mortgage rate of 6.14% (which is on the lower end):

A borrower making $100K with 20% down, no debt, on a 30yr amortization:

– September 2016 qualifies for a $796K mortgage at 2.34%

– February 2022 qualifes for a $598K mortgage at 5.25%

– Today qualifies for a $466K mortgage at 8.14%

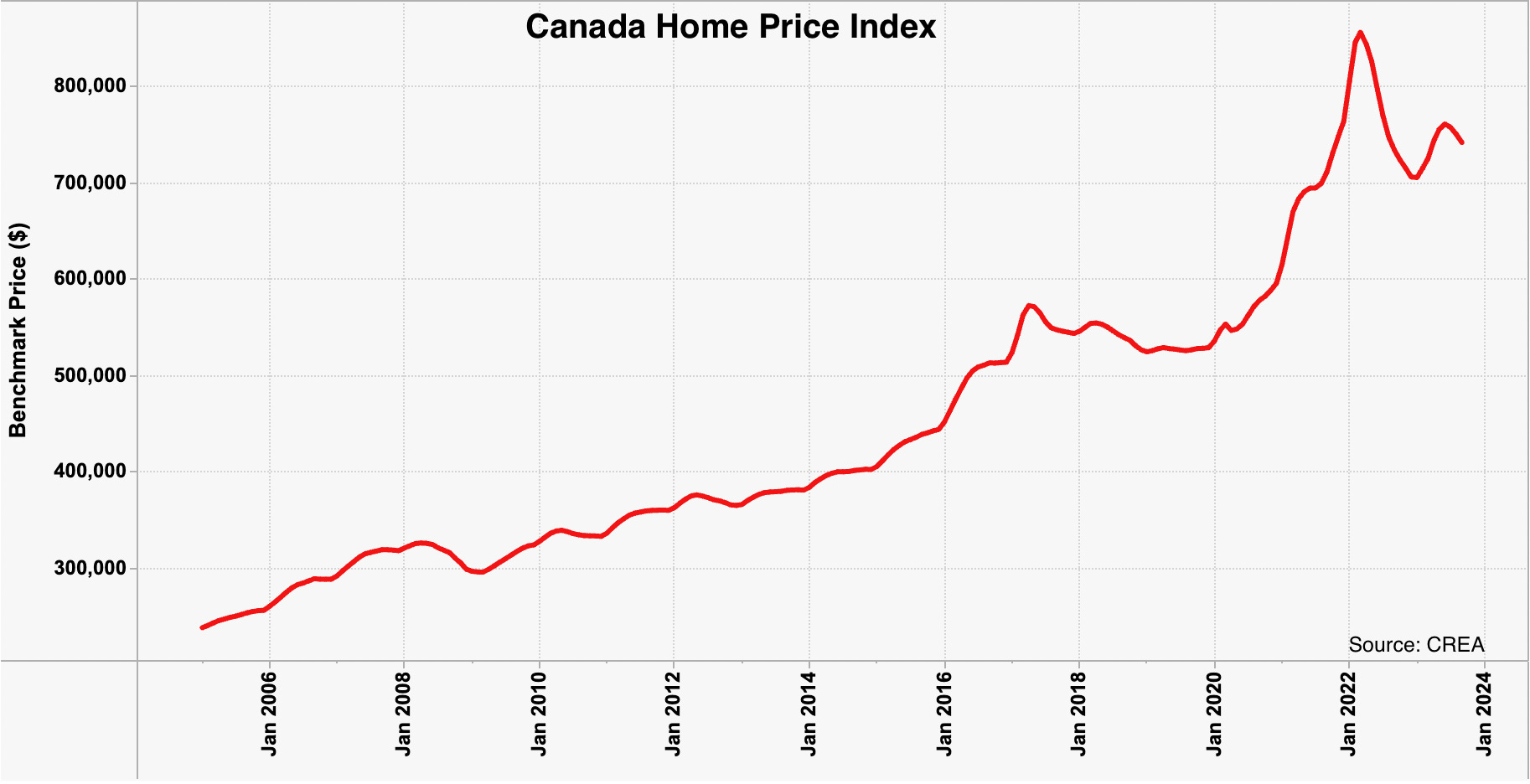

So yes, it seems reasonable to expect this chart to roll lower.

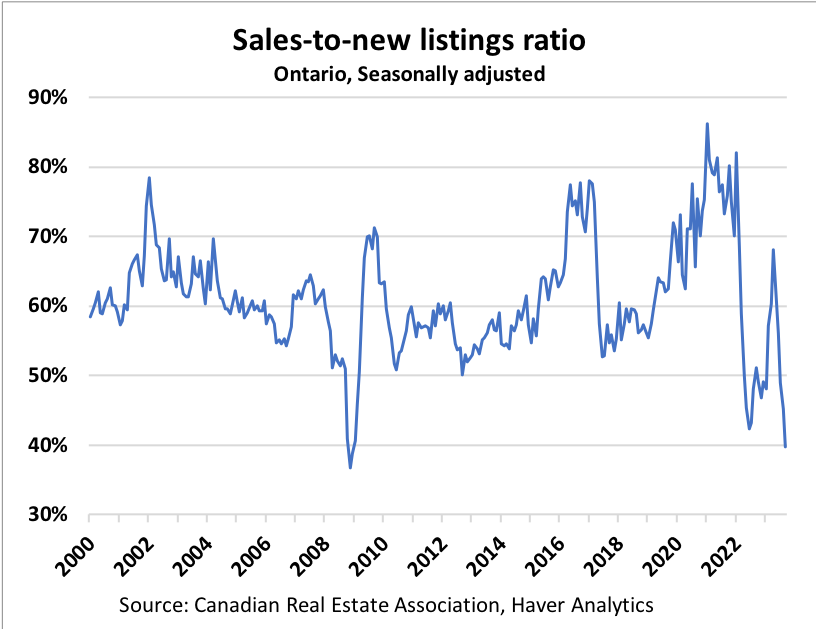

Keep in mind this index has a heavy weighting towards Ontario, and as we know, real estate is hyper local. Ontario, was not only at the centre of the speculative frenzy, but now appears to be in the eye of the storm. The Sales-to-new listings ratio for Ontario is now at levels last seen during the depths of the Financial Crisis.

So, like I said, rates need to fall in a hurry to release some of the pressure. Every month that ticks by more Canadians get sucked up into vortex of higher rates. According to recent financials at the big 5 banks, from now until August 2024 an average of 70,000 mortgages will renew each month at significantly higher mortgage rates. That number jumps to about 105,000 mortgages per month from August 2024 onwards.

Nearly a 100,000 Canadian households each month enduring a doubling, or more, on their mortgage rate. What do you think that does to discretionary spending?

And to think Tiff Macklem at the BoC was out this week saying they’re not expecting a recession in Canada.